Overview

Even though cashless payments are becoming increasingly prevalent, there are still many instances where traditional banking services are essential – whether it’s for sending money, withdrawing cash, or arranging a loan. In fact, you typically need an account just to receive your salary or pay your rent. What might surprise some is the variety of banking institutions we have.

There are several national mega banks, numerous regional and local banks, as well as many online banks. The lines between these are a bit blurred in some cases, but these are the three main categories for practical purposes.

Mega banks

When most people outside Japan, or even new residents, think of a “bank,” their minds likely jump to the large “Mega-banks.” These are the titans of the financial world here, with their imposing, modern branches dotted across major cities and beyond. They offer a comprehensive suite of services, ranging from standard savings and checking accounts to complex financial products like mortgages and investment vehicles, catering to both individual and corporate clients. Their extensive ATM networks and robust online banking platforms make them incredibly convenient for everyday use.

Many older and/or conservative people feel that megabanks are somehow “safer” than the other types of banks. This has no basis in reality since all banks are required to follow the same rules and to have the same deposit insurance.

Examples of Mega Banks:

- Mitsubishi UFJ Bank (MUFJ) (三菱UFJ銀行)

- Sumitomo Mitsui Banking Corporation (SMBC) (三井住友銀行)

- Mizuho Bank (みずほ銀行)

- Japan Post Bank (JP Bank) (ゆうちょ銀行) – Run by the post office – See more about this below.

- Resona Bank (れぞな銀行)

Regional Banks

Moving down in scale, we have the “Regional Banks” (地方銀行 – chihou ginkou). As their name suggests, these institutions operate primarily within specific prefectures or regions. They often possess a deeper understanding of the local economy and community needs, which can translate into more tailored services for residents and local businesses. Many people appreciate their more “hometown” or familiar feel compared to the larger institutions.

Regional banks are often willing to give loans to people that megabanks aren’t, and sometimes have better interest rates and lower fees.

Examples of Regional Banks:

- Chiba Bank (千葉銀行)

- Yokohama Bank (横浜銀行)

- Tokyo Star Bank (東京スター銀行)

- Fukuoka Bank (福岡)

A distinct category includes “Shinkin Banks” (信用金庫 – shinyou kinko) and “Credit Cooperatives” (信用組合 – shinyou kumiai). These are unique in that they are member-owned financial cooperatives, similar to Credit Unions in the US. Their core mission is to support and foster the prosperity of their local communities and small to medium-sized enterprises (SMEs). They are generally smaller than regional banks and are often lauded for their community-centric approach and supportive services for local entrepreneurs.

Often government loans and grants (f.e. small business support programs) require the use of a these institutions.

- Tokyo Shinkin Bank (東京信用金庫)

- Setagaya Shinkin Bank (世田谷信用金庫)

- Hyogo Shinkin Bank (兵庫信用金庫)

- Kobe Shinkin Bank (神戸信用金庫)

Net Banks

In recent years, “Internet-only Banks” (ネット銀行 – netto ginkou) have seen a significant surge in popularity, particularly among a younger demographic and those who prioritize digital convenience. Operating without physical branches, they leverage technology to offer services entirely online. This often results in competitive advantages like lower transaction fees, more attractive interest rates on deposits, and highly intuitive mobile applications, making them a preferred choice for many digital-savvy users.

A recent phenomenon is the emergence of Banking as a Service (BaaS) and “Virtual banks”. This allows companies without a banking license or infrastructure to launch a bank with their own branding and financing. These include (for example) JRE Bank and Takashimaya Neobank.

Examples of Online Banks:

- Sony Bank (Moneykit) (ソニー銀行)

- SBI Sumishin Net Bank / NEOBANK (SBI住信SBIネット銀行)

- Seven Bank (セブン銀行) – (Run by 7&i, the holding company of the popular 7-11 convenience store chain).

- Rakuten Bank (楽天銀行)

- JRE Bank (Run by Japan Rail East with the infrastructure provided by Rakuten Bank)

- PayPay bank (Previously Japan Net Bank) (PayPay銀行)

- au Jibun Bank (auじぶん銀行)

- Aeon Bank (イオン銀行)

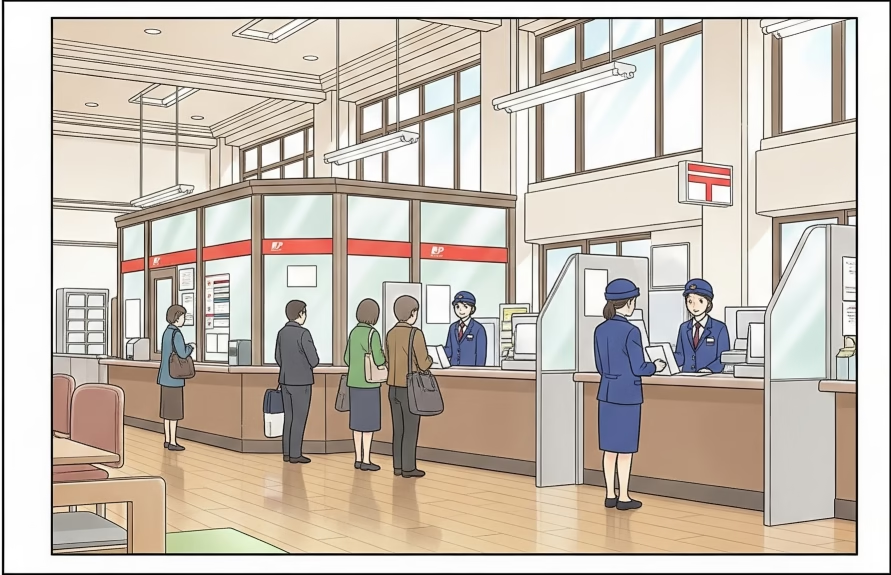

More about Japan Post Bank

Japan Post bank started as the “Postal Savings” system in 1875, based on a similar system that was in place in the UK. The primary goal at the time was to provide a simple, secure, and universally accessible means for the public to save money.

We listed this in the section above, and it is a mega bank, but it is a bit different from the others. Japan Post Bank is distinctive because it was historically an arm of the national postal service, its immense network is unparalleled. Thanks to its origins, Japan Post Bank has service points (or at least ATMs) in virtually every post office across the archipelago, making it incredibly accessible, even in the most remote rural areas where other banking options might be scarce.

Investment Banks

Investment banks (証券) are also common, but not really considered “banks” in Japan. These allow you to trade stocks and bonds, etc., but require a separate type of license, and are often linked to a “normal” consumer bank.

Examples:

- Nomura Shoken (野村証券)

- Rakuten Securities (楽天証券)

- Mitsubishi UFJ eSmart Securities (三菱UFJ eスマート証券) (Previously: kabu.com)

- SBI Securities (SBI証券)

For example, Rakuten Securities is a separate company set up by Rakuten that lets you set up investment accounts. You can set up a normal Rakuten account at Rakuten bank, an investment account at Rakuten securities, and link them for easier transfers. The same situation applied to SBI and other companies.

Personal Experience

I’ve had accounts at 2 of the commercial megabanks, numerous net banks, one regional bank, and JP Post.

Summary

This has been a brief overview of the diverse banking landscape here in Japan. Each type of institution serves a particular niche and contributes to the overall financial ecosystem. It’s quite fascinating when you consider the unique roles they each play in our society.

- Megabanks will have the most branches around the country, and you can walk into one any time you need to do some paperwork, etc.

- Regional and local banks will often offer your better deals on interest rates, etc., but may not have ATMs all around the country.

- Online banks will generally offer the best deals, and the best online banking, but have few or no physical branches. The other banks also have online banking, though the available features often lag behind the online banks.

- Japan Post Bank has the most locations of any bank in Japan.

Comments